Especially now in Corona times some of us are thinking about buying a boat in the Netherlands. If it is a used boat on which the VAT has already been paid, it only needs a corresponding receipt to be on the safe side.

However, if VAT has not yet been paid on the object of desire, non-EU citizens like us can defer the VAT payment when buying a boat in the Netherlands and thus significantly reduce it.

Not being part of the EU has undeniable advantages and disadvantages. One advantage is that VAT in Switzerland is much lower than in the EU, even if this is not reflected in the prices of goods. Since 2018, our VAT rate has been 7.7%. Compared to the Netherlands with a whopping 21%, this quickly adds up to a larger amount, especially for a boat that never comes cheap.

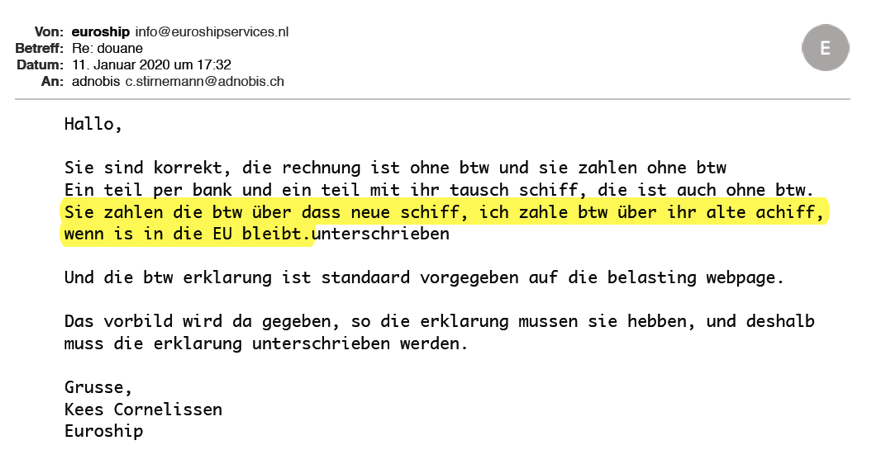

But we have discussions with customs regarding the VAT of our former Adnobis.

This because Kees Cornelissen has not kept to our agreements.

ADNOBIS

First of all the formalities:

For non-EU citizens there is the possibility to defer the VAT liability in the EU by temporarily exporting and re-importing a boat. In the case of boats, this Dutch 21 % on the purchase amount quickly runs into thousands, which is why many are happy to make use of this option.

To do this, the seller has an Agentschap Douane, a company specializing in customs formalities, fill out the appropriate documents. The buyer reports to customs and indicates when he intends to export the boat to international waters. If the boat has AIS, it becomes easier, as customs can follow its path in real time. One sails to a designated buoy, takes photos of the buoy, the engine hours before departure and after return and with this evidence meets one of the friendly customs officers who fills out and confirms the necessary paperwork.

Thereupon, one is allowed to sail the boat in the EU for 18 months, after which it can be exported and imported again. In total this is possible 10 times. If the boat is resold to an EU citizen in the meantime, VAT must be paid on the purchase price. If it is not resold, VAT must be paid on the value depreciated after 15 years. The receipts for the value-preserving work done on the boat in the meantime, including VAT, must be kept, because this VAT may be deducted in the final payment.

We received these explanations in summer 2021 from a really very helpful and friendly customs officer.

So far so good. We had already used this procedure with Adnobis and planned to do the same with Caro.

It was agreed with Cornelissen that he would pay the VAT when he took over the exchanged Adnobis and that the VAT of the Caro was logically our responsibility.

Of course, we have that in writing. But . . all written agreements are only of use if both parties stick to them.

In reality, Kees Cornelissen refused to properly fill out the paperwork needed for the customs agency for the Caro. We were able to get around this obstacle and the Caro is on its way with valid customs papers and stands up to any inspection. In fact, we got a very nice confirmation of this on the occasion of a customs check in Zoutkamp, when we were visited out of the blue by two smart female customs officers. I wonder if they were sent to us? And by whom?

But what Kees Cornelissen has allowed himself with the resale of our Adnobis, unfortunately cries out again for a walk before the judge.

In May 2020, the Adnobis was transferred to a Dutch buyer via Sleeuwijk Yachting Makelaars. The excerpt from the purchase agreement clearly shows that Mr. Cornelissen demanded VAT from the buyer and the buyer paid it.Why he did not pay it through us in the name of Adnobis as agreed, we can vividly imagine, but only he knows for sure.

Customs, which has nothing to do with Mr. Cornelissen, now demands this VAT from us, which is logical and correct. On the other hand, VAT cannot be charged twice on the same thing and for the Adnobis it has already been charged by Cornelissen.

We will report how the matter turns out. We are talking about almost 60,000 euros.

CARO - tax fraud proposal ?

We find what Mr. Cornelissen has done with the VAT statement of Adnobis bad enough. His proposal concerning CARO was a firecracker.

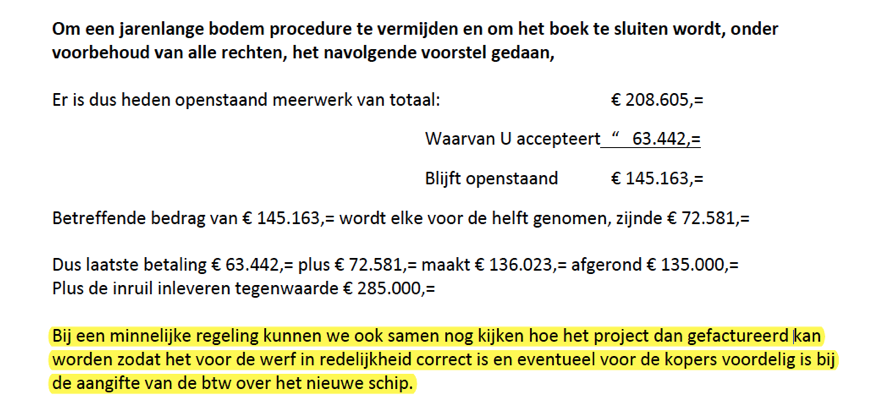

We remember. Kees Cornelissen is still of the opinion that he is owed almost 150,000 euros for additional work, even though he can neither explain what we would have ordered nor what exactly he delivered more of.

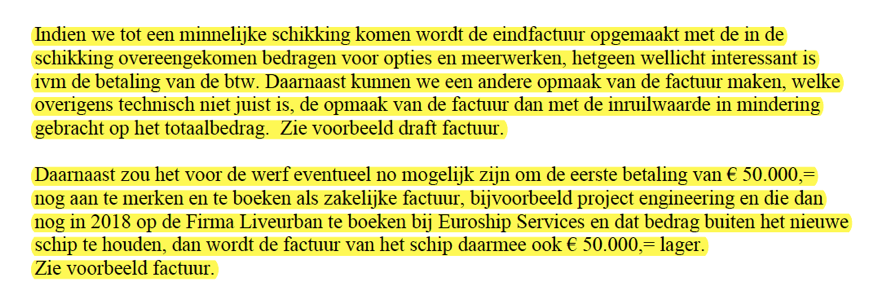

In order to still get his unearned money, he suggested that he would issue an invoice for tax purposes, which would be lower than what we would pay. We would then pay him the amount saved on VAT and thus have a zero-sum game.

You can look at it however you want. In our eyes this is a tax fraud proposal.

What Kees Cornelissen completely ignores in his disreputable proposal is that we do not owe him, but he owes us. We have paid what was contractually agreed. We have even paid for what he has demonstrably not delivered.

If we accepted this dubious proposal, according to Cornelissen, it might be advantageous for us when he hands over the boat. He writes: "In case of an amicable agreement, the handover and use of the boat will go more smoothly, you can receive further sailing instructions and explanations and instructions on the technical equipment and its proper use."

Here what Kees Cornelissen wrote on the subject.

Click on the document enlarges it.

And here are his sample calculations of how he intended to handle it:

Although in this case nothing can really surprise us anymore, we are still amazed when even Cornelissen's lawyer at the time, Frits Hommersom, in his letter of November 27, 2019, inquires why we have not responded to this proposal.

The rhetorical question arises: Is tax fraud not prosecutable in the Netherlands?

Diese Website verwendet keine Cookies. Bitte lesen Sie unsere Datenschutzerklärung für Details.